Author of Startup Ninja

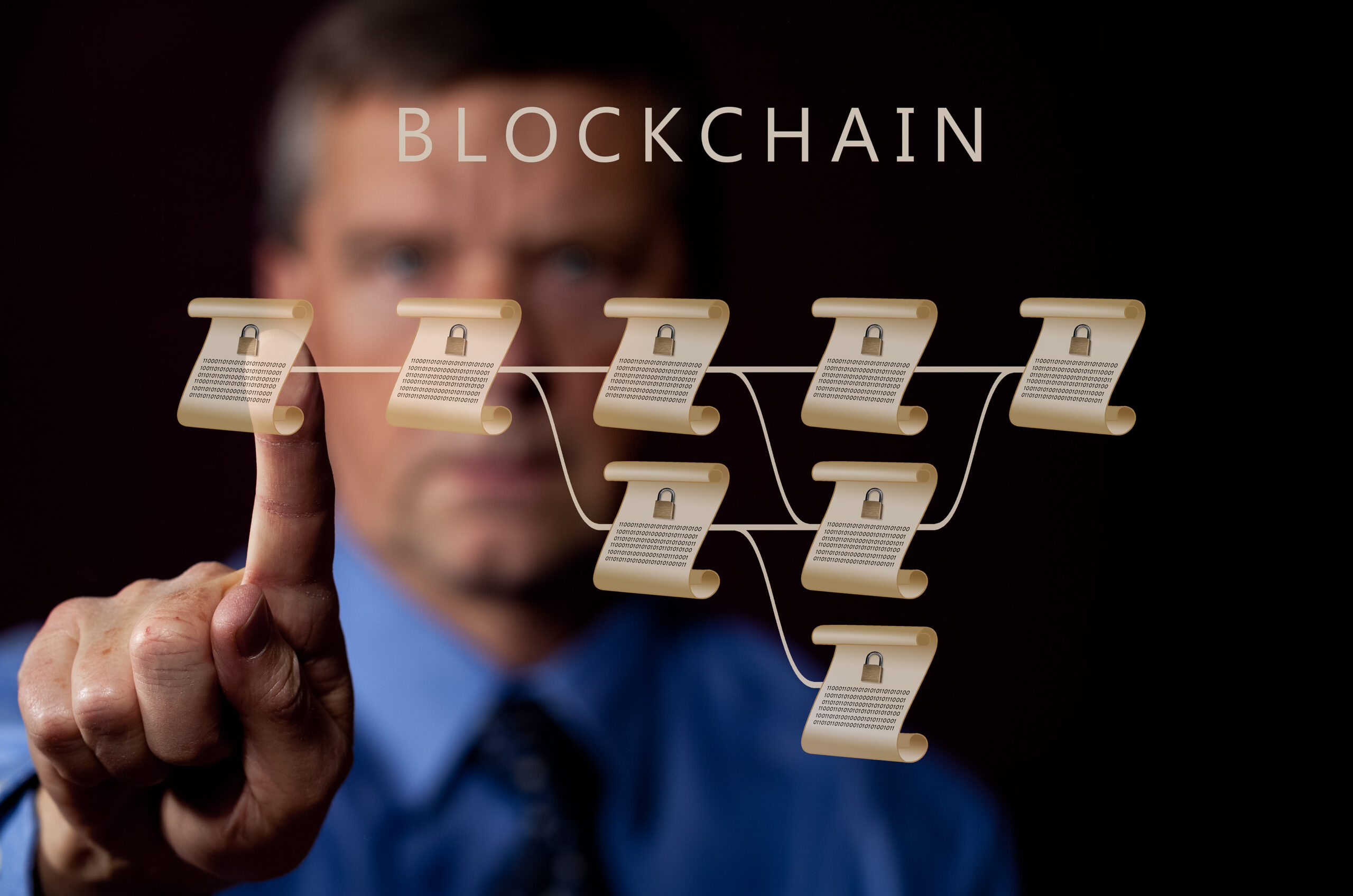

The blockchain concept was described first by David Chaum in the early 1980s, developed further by Stuart Haber and W. Scott Stornetta in the early 1990s, and conceptualised as a decentralised system by the mythical Satoshi Nakamoto in 2008. It is nothing new.

Blockchain technology has been used as the underpinning of cryptocurrencies since 2009 when Nakamoto first implemented Bitcoin, where a blockchain provides the public ledger for all transactions. This concept has been replicated thousands of times as creating a cryptocurrency is relatively easy. According to Coinmarketcap, there were over 8,000 cryptocurrencies – or altcoins – listed on its website at the end of 2021. However, the vast majority of these have very little market capitalisation and are not traded widely.

It is important to note that the future of cryptocurrency and its potential real-world applications is a highly debated topic in the financial and technology industries.

Why not!

One argument against the long-term viability of cryptocurrency is the lack of widespread adoption and use in everyday transactions. Despite the increasing acceptance of cryptocurrencies by merchants and businesses, the vast majority of transactions still occur using traditional fiat currencies. Additionally, many individuals and institutions remain sceptical of the security and stability of cryptocurrencies, leading to a lack of trust in their potential as a reliable form of currency.

Another issue is the extreme volatility of the cryptocurrency market. The value of many cryptocurrencies can fluctuate wildly in a short period of time, making them a risky investment. This volatility can also make it difficult for businesses to accept cryptocurrencies as a form of payment, as the value of the currency may change significantly between the time of a transaction and the time the business needs to convert the cryptocurrency into fiat currency to cover its own expenses.

Additionally, there are concerns over the lack of regulation in the cryptocurrency market. Because of the decentralised nature of cryptocurrency, it operates outside of government oversight and control. This can lead to potential issues such as money laundering and fraud.

The energy consumption of the cryptocurrency industry is also a significant concern. The process of “mining” for new cryptocurrency requires significant computational power, which in turn requires large amounts of energy. This has led to criticism that the cryptocurrency industry is contributing to climate change and other environmental issues.

The lack of scalability of the current blockchain technology is also an issue. The Bitcoin blockchain, for example, can only handle around 7 transactions per second, while Visa, the world’s largest payment processor, can handle up to 24,000 transactions per second. This issue could lead to transaction delays and increased costs as the number of users on the network increases.

While cryptocurrency has been gaining popularity in recent years, it still faces many challenges in terms of adoption, stability, regulation, and scalability. Until these issues are addressed, it is unlikely that cryptocurrency will have significant real-world applications. It is possible that the crypto industry will evolve and resolve these problems, but for now, it is considered to be a flash in the pan by many experts.

However…

However, blockchain technology has the potential for other real-world applications which can provide added value over existing solutions.

Supply Chain Management: Blockchain can be used to create a tamper-proof, transparent and immutable record of transactions within a supply chain. This can improve traceability and accountability, reducing the risk of fraud and errors.

Healthcare: Blockchain can be used to securely store and share patient health data, ensuring that only authorised parties have access to it. It can also be used to track the movement of drugs and medical equipment throughout the supply chain, reducing the risk of counterfeit products.

Digital Identity: Blockchain can be used to create a secure, decentralised system for storing and verifying personal information, such as identity documents. This can help to prevent identity fraud and improve access to financial and other services.

Smart Contracts: Blockchain technology can be used to create smart contracts, which are self-executing contracts with the terms of the agreement between buyer and seller being directly written into lines of code. This can automate and streamline legal and business processes, reducing the need for intermediaries and increasing efficiency.

Voting: Blockchain can be used to create a secure and transparent system for voting, which can help to increase voter turnout and reduce the risk of voter fraud.

Energy: Blockchain can be used to create a peer-to-peer energy trading system. This can enable individuals and businesses to buy and sell energy directly with each other, increasing competition and reducing costs.

Charity and donation: Blockchain technology can be used to create a transparent and accountable system for tracking donations and aid distribution. This can increase trust and transparency in the charitable sector and help to ensure that donations reach the intended recipients.

Real Estate: Blockchain can be used to digitise ownership of real estate assets, making it possible to buy, sell, and transfer property without intermediaries, and also to create a tamper-proof record of all transactions on the property, making it easier to verify ownership, and reducing the time and costs associated with property transactions.

These are just a few examples of the many potential real-world applications of blockchain technology. As the technology continues to evolve and improve, it is likely that new and innovative uses for blockchain will be developed, far away from today’s hype surrounding cryptocurrencies.

David Tee is a tech junkie, innovation, world traveller expert and author of Startup Ninja.